Tuna fishery

The following profile provides the socioeconomic context of the tuna fishery in British Columbia. It includes an overview of the commercial and recreational sectors. This overview is based on data collected from DFO commercial harvest logbooks and sale slips, public reports, and DFO surveys on harvest prices and recreational fisheries.

Long text version

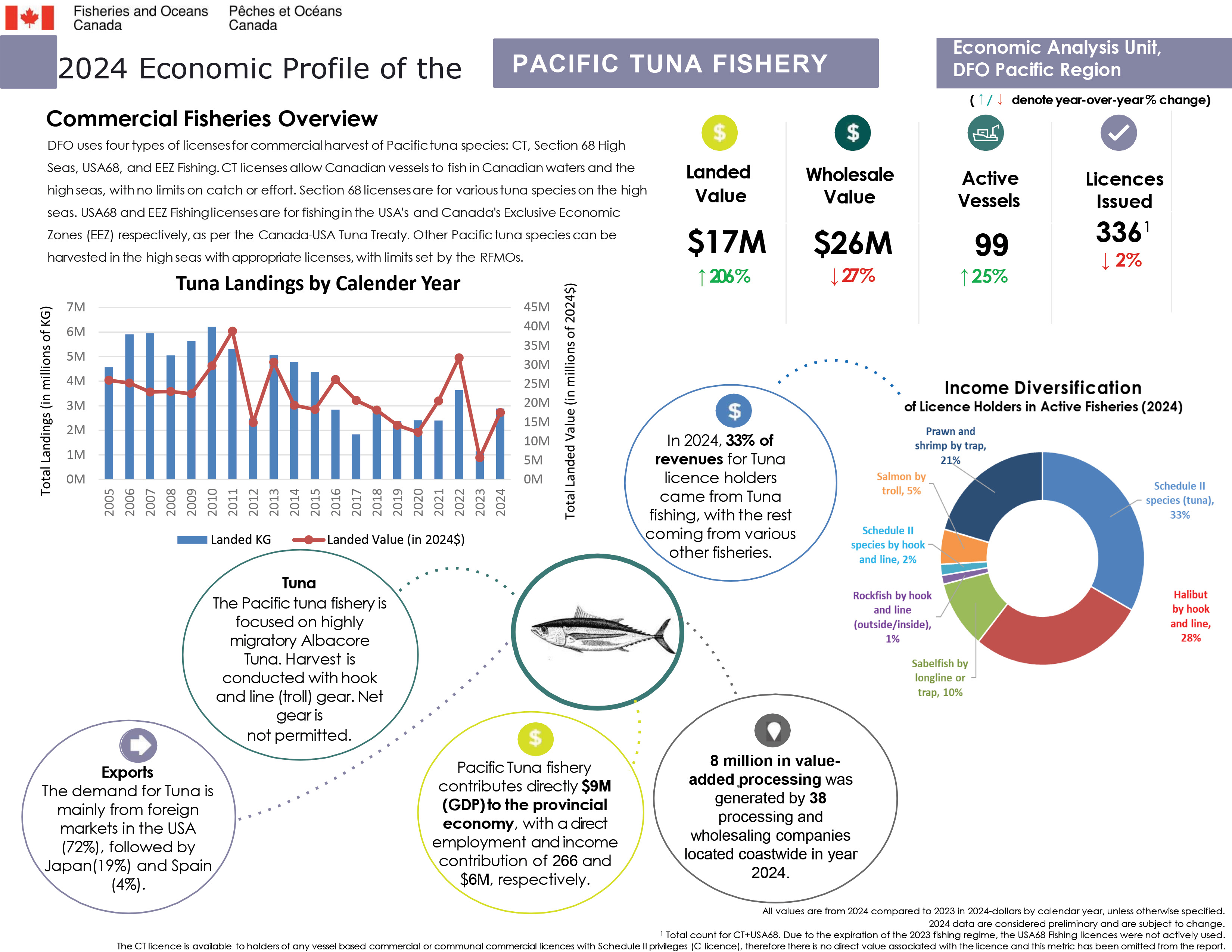

Commercial fisheries overview

DFO uses four types of licenses for commercial harvest of Pacific tuna species: CT, Section 68 High Seas, USA68, and EEZ Fishing. CT licenses allow Canadian vessels to fish in Canadian waters and the high seas, with no limits on catch or effort. Section 68 licenses are for various tuna species on the high seas. USA68 and EEZ Fishing licenses are for fishing in the USA's and Canada's Exclusive Economic Zones (EEZ) respectively, as per the Canada-USA Tuna Treaty. Other Pacific tuna species can be harvested in the high seas with appropriate licenses, with limits set by the RFMOs.

All values are from 2024 compared to 2023 in 2024-dollars by calendar year, unless otherwise specified.

Key metrics of the Pacific Tuna Fishery, all values are from 2024 in 2024 dollars:

- Landed value ($17M), increased by 206% since 2023.

- Wholesale value ($26M), decreased by 27% since 2023.

- Active vessels (99), increased by 25% since 2023.

- Licences issued (336, decreased by 2% since 2023). Licence eligibilities represents the number of issued licences.

2024 data are considered preliminary and are subject to change.

Total count for CT+USA68. Due to the expiration of the 2023 fishing regime, the USA68 Fishing licences were not actively used.

The CT licence is available to holders of any vessel based commercial or communal commercial licences with Schedule II privileges (C licence) therefore there is no direct value associated with the licence and this metric has been omitted from the report.

Tuna landings (in kilograms) and value (in 2024 dollars) by calendar year

Landed kilograms

- 2005 – 4.57M KG

- 2006 – 5.91M KG

- 2007 – 5.95M KG

- 2008 – 5.05M KG

- 2009 – 5.63M KG

- 2010 – 6.22M KG

- 2011 – 5.32M KG

- 2012 – 2.48M KG

- 2013 – 5.07M KG

- 2014 – 4.78M KG

- 2015 – 4.38M KG

- 2016 – 2.84M KG

- 2017 – 1.84M KG

- 2018 – 2.72M KG

- 2019 – 2.39M KG

- 2020 – 2.41M KG

- 2021 – 2.40M KG

- 2022 – 3.64M KG

- 2023 – 1.14M KG

- 2024 – 2.88M KG

Landed value (in 2024$)

- 2005 - $26.0M

- 2006 - $25.2M

- 2007 - $22.9M

- 2008 - $23.0M

- 2009 - $22.4M

- 2010 – $29.7M

- 2011 - $38.8M

- 2012 - $14.9M

- 2013 - $30.7M

- 2014 - $19.4M

- 2015 - $18.3M

- 2016 - $26.2M

- 2017 - $20.7M

- 2018 - $18.2M

- 2019 - $14.2M

- 2020 - $12.3M

- 2021 - $20.5M

- 2022 - $31.8M

- 2023 - $5.7M

- 2024 - $17.5M

Income diversification of licence holders in active fisheries (2024)

In 2024, 33% of revenues for tuna licence holders came from tuna fishing, with the rest coming from halibut (28%), prawn and shrimp (21%), sablefish (10%), salmon by troll (5%), schedule ii (2%), and rockfish (1%).

Exports: The demand for Tuna is mainly from the USA (72%), followed by Japan (19%) and Spain (4%).

$8M in value-added processing was generated by 38 processing and wholesaling companies located coastwide in year 2024.

Pacific Tuna fishery directly contributes $9M (GDP) to the provincial economy, with a direct employment and income contribution of 266 and $6M, respectively.

The Pacific tuna fishery is focused on highly migratory Albacore Tuna. Harvest is conducted with hook and line (troll) gear. Net gear is not permitted.

The tidal water recreational fishing survey data is not available for 2024. Please see the 2023 infographic for recreational values:

Data

The commercial data and the recreational data that informed this work can be downloaded here.

- Date modified: